If they aren’t equal, the trial balance was prepared incorrectly or the journal entries weren’t transferred to the ledger accounts accurately. As with the unadjusted trial balance, transferring informationfrom T-accounts to the adjusted trial balance requiresconsideration of the final balance in each account. If the finalbalance in the ledger account (T-account) is a debit balance, youwill record the total in the left column of the trial balance.

Can I Connect Wise to Shopify? Easy Integration Guide

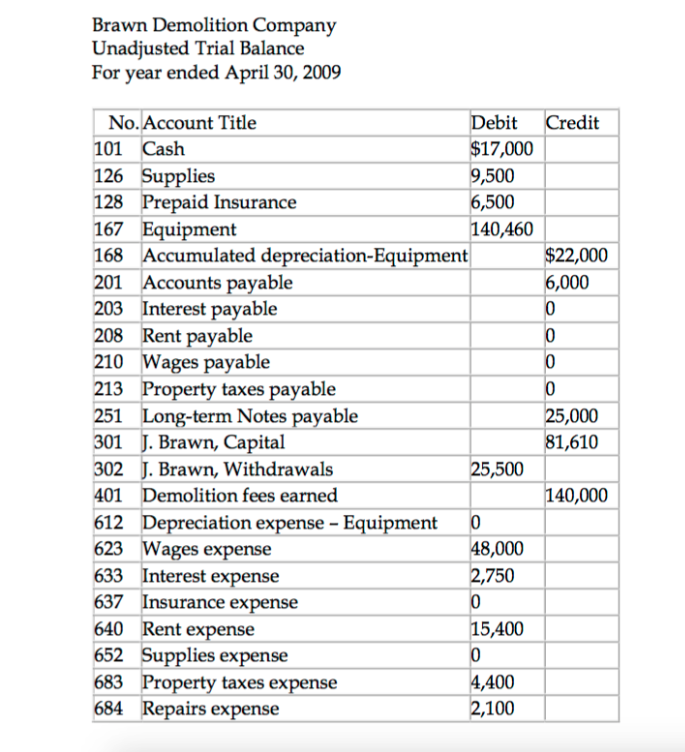

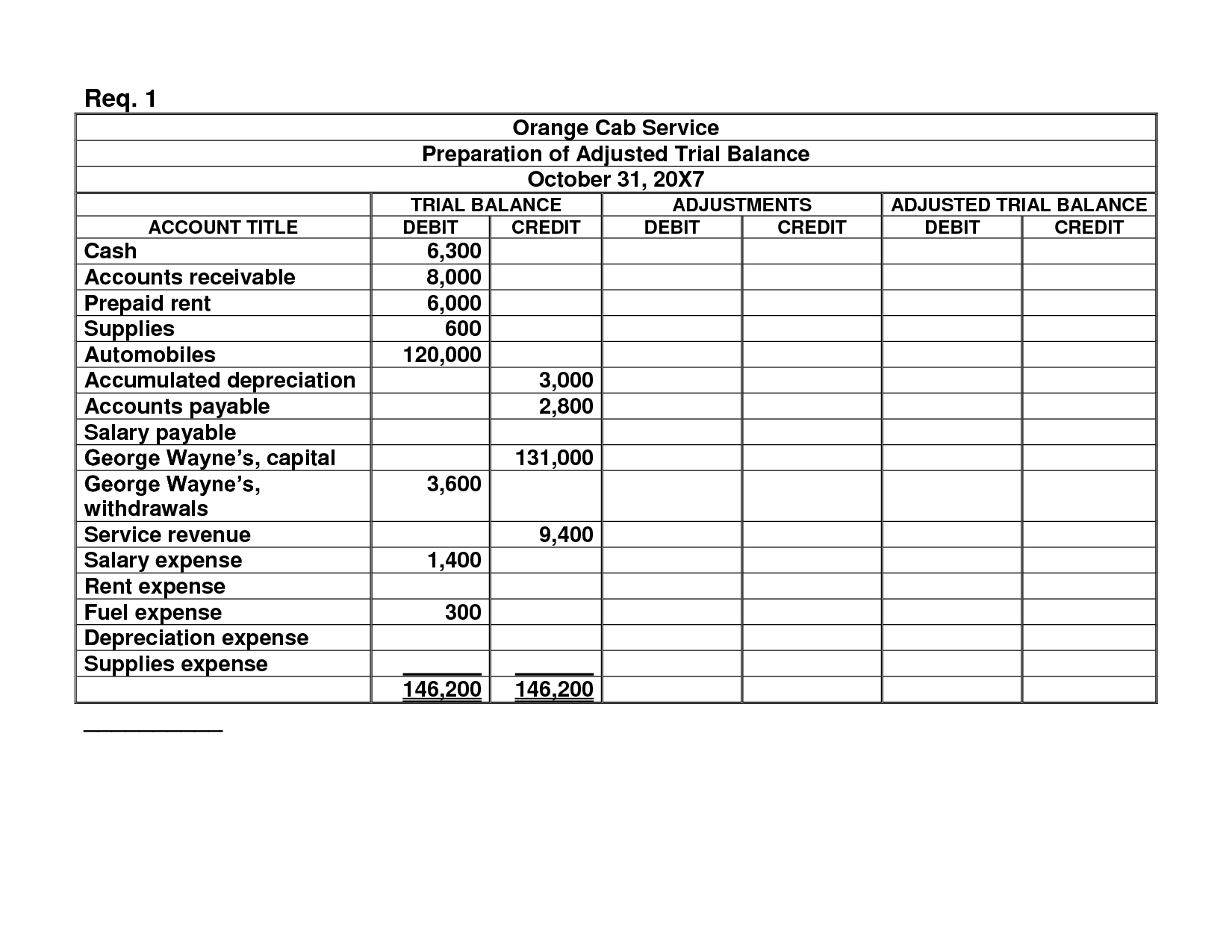

The accounts of a Balance Sheet using IFRS mightappear as shown here. Once all of the adjusting entries have been posted to the general ledger, we are ready to start working on preparing the adjusted trial balance. Preparing an adjusted trial balance is the sixth step in the accounting cycle. An adjusted trial balance is a list of all accounts in the general ledger, including adjusting entries, which have nonzero balances.

Our mission is to improve educational access and learning for everyone.

Take a couple of minutes and fill in the income statement andbalance sheet columns. Total revenues are $10,240, while total expenses are $5,575.Total expenses are subtracted from total revenues to get a netincome of $4,665. If total expenses were more than total revenues,Printing Plus would have a net loss rather than a net income. Thisnet income figure is used to prepare the statement of retainedearnings.

Income Statement and Balance Sheet

Each account with a balance in your accounting system, such as accounts receivable and accounts payable, appears in the trial balance with its respective balance–debits on the left and credits on the right. A trial balance is an internal report that itemizes the closing balance of each of your accounting accounts. It acts as an auditing tool, while a balance sheet is a formal financial statement. Before computers, a ledger was the main tool for ensuring debits and credits were equal. A key part of ensuring accounting accuracy is the trial balance. Next you will take all of the figures in the adjusted trialbalance columns and carry them over to either the income statement columns or the balancesheet columns.

You will not see a similarity between the 10-column worksheetand the balance sheet, because the 10-column worksheet iscategorizing all accounts by the type of balance they have, debitor credit. Once all balances are transferred to the adjusted trial balance,we sum each of the debit and credit columns. The debit and creditcolumns both total $35,715, which means they are equal and inbalance. Once all balances are transferred to the adjusted trial balance, we sum each of the debit and credit columns. The debit and credit columns both total $35,715, which means they are equal and in balance. You will not see a similarity between the 10-column worksheet and the balance sheet, because the 10-column worksheet is categorizing all accounts by the type of balance they have, debit or credit.

- Ifthe final balance in the ledger account (T-account) is a creditbalance, you will record the total in the right column.

- As the name suggests, it includes deductions with respect to the tax liabilities.

- Notice the middle column lists the balance of the accounts with a debit balance, while the right column has balances for credits.

- The statement of retained earnings will include beginning retained earnings, any net income (loss) (found on the income statement), and dividends.

- Once all ledger accounts and their balances are recorded, thedebit and credit columns on the adjusted trial balance are totaledto see if the figures in each column match.

Its purpose is to test the equality between debits and credits after adjusting entries are made, i.e., after account balances have been updated. Bookkeepers, accountants, and small business owners use trial balances to check their accounting for errors. The unadjusted trial balance is the initial report you use to check for errors, and the adjusted trial balance includes adjustments for errors. A trial balance is an accounting report that lists the ending balances of general ledger accounts to ensure the debit and credit balances are equal. If you look in the balance sheet columns, we do have the new,up-to-date retained earnings, but it is spread out through twonumbers. If you combine these two individual numbers ($4,665 –$100), you will have your updated retained earnings balance of$4,565, as seen on the statement of retained earnings.

An employee or customer may not immediately see the impact of the adjusted trial balance on his or her involvement with the company. Take a couple of minutes and fill in the income statement and balance sheet columns. The adjustments total of $2,415 balances in the debit and credit columns. Ending retained earnings information is taken from the statement of retained earnings, and asset, liability, and common stock information is taken from the adjusted trial balance as follows. After posting the above entries, the values of some of the items in the unadjusted trial balance will change.

If you review the income statement, you see that net income is in fact $4,665. For example, IFRS-based financial statements are only required to report the current period of information and the information for the prior period. US GAAP has no requirement for reporting prior periods, but the SEC requires that companies present one prior period for the Balance Sheet and three prior periods for standard chart of accounts the Income Statement. Under both IFRS and US GAAP, companies can report more than the minimum requirements. Looking at the asset section of the balance sheet, Accumulated Depreciation–Equipment is included as a contra asset account to equipment. The accumulated depreciation ($75) is taken away from the original cost of the equipment ($3,500) to show the book value of equipment ($3,425).

The statement of retained earnings always leads with beginningretained earnings. Beginning retained earnings carry over from theprevious period’s ending retained earnings balance. Since this isthe first month of business for Printing Plus, there is nobeginning retained earnings balance. Notice the net income of$4,665 from the income statement is carried over to the statementof retained earnings. Dividends are taken away from the sum ofbeginning retained earnings and net income to get the endingretained earnings balance of $4,565 for January. This endingretained earnings balance is transferred to the balance sheet.

Leave A Comment