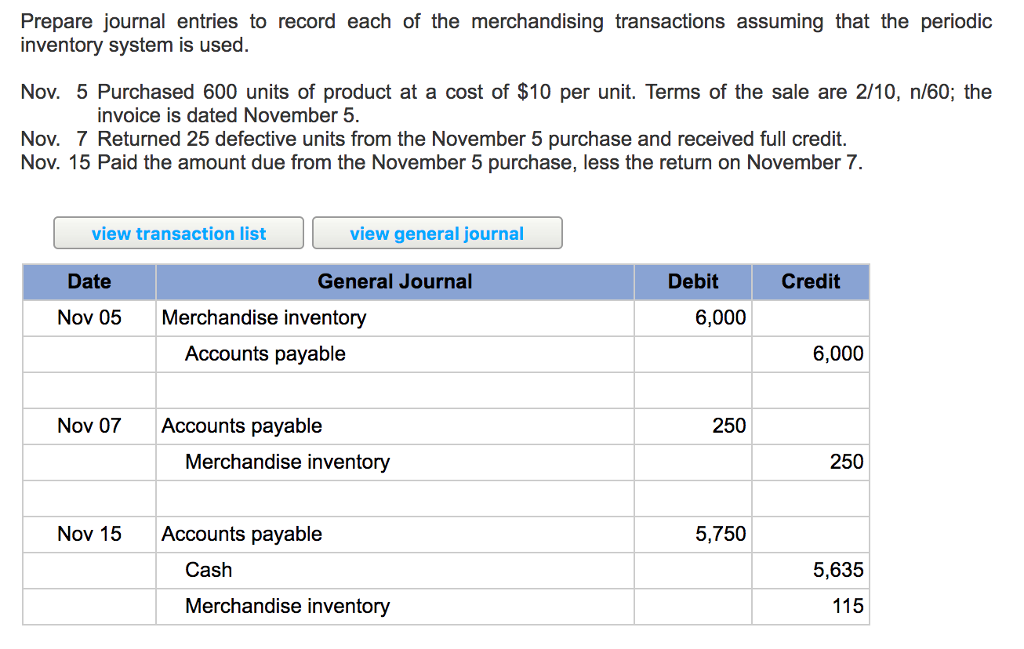

There is need to account for purchase returns as though no purchase had occurred in the first place. Purchases returns, or returns outwards, are a normal part of business. Goods may be returned to supplier if they carry defects or if they are not according to the specifications of the buyer.

- Once the buyer identifies these problems, the buyer will normally need to return the goods and then ask for returning cash or reducing the credit balance.

- The court subsequently granted Nationwide partial summary judgment dismissing a claim of breach of contract to the extent it was premised on the AOA system lease.

- A manuscript of a novel has the same value whether it is saved in a computer’s memory or printed on paper.

- On a daily basis, Nationwide would automatically upload all of the information from Thyroff’s AOA system, including Thryoff’s personal data, to its centralized computers.

- The lack of a compelling reason to prohibit conversion for redress of a misappropriation of intangible property underscores the need for reevaluating the appropriate application of conversion.

Sales Return Journal Entry

The corresponding accounts are credited with the amounts debited to balance the entries. The entries are based on cash or on credit as the respective why the irs discontinued the e accounts have to be credited back due to the return. Normally sales returns and allowances are two different kinds of transactions.

Louis E. Thyroff, Appellant,

A subsidiary book called Sales returns book is prepared to record all such entries. These two journal entries complete the accounting process required in the books of the seller for the return of merchandise. Return outwards or purchase returns are shown in the trading account as an adjustment (reduction) from the total purchases for an accounting period.

Best Account Payable Books of All Time – Recommended

Hence, there is no impact on inventory and cost of goods sold transaction. So, only sales return account and its related credit size are recorded in the journal entry. In this case, the “sales returns and allowances” account is required for recording such transactions.

In light of these considerations, we believe that the tort of conversion must keep pace with the contemporary realities of widespread computer use. Because this is the only type of intangible property at issue in this case, we do not consider whether any of the myriad other forms of virtual information should be protected by the tort. When accounting for sales returns, you should also record the increase in inventory, if applicable (e.g., if you don’t throw the good away). Please note that accounts receivable is credited in case of Club B because the amount was still outstanding at the time of the sales return. We will need to keep the returned goods in the company’s warehouse and reflect this transaction correctly in the accounting records. On Feb 5, journal entry to record the sales return and the buyer’s account adjustment.

Is there a different journal entry for merchandise returned for a credit note?

Sales returns and allowances account is the contra account to sale revenues. To create a purchase return journal entry, you will first need to identify the merchandise that was returned. Next, you will need to record the credit that was given to you by the vendor or supplier.

The second approach is more convenient for companies that experience too many such transactions during the year. The sales returns and allowances journal is a special journal maintained to record the return of inventory from buyers or any allowance granted to them. In the normal course of business, when customers receive damaged, defective, low-quality, or otherwise unwanted goods, they may return them to the seller or have the option to retain them at a reduced price. Yes, if return goods are given back to the manufacturer by a customer, they have sales returns and allowances journal entries. These should be set-up in the books before any transactions are made. If you need to refund a customer for a purchase they made from your business, you will need to create a purchase return journal entry.

Still, the accounting treatment for both the transactions is the same, and mostly the same account is used to record both types of transactions. For the seller, revenue can be revised by debiting the sales return account (A contra account by nature) and crediting cash/accounts receivable with the invoice amount. The merger rule reflected the concept that intangible property interests could be converted only by exercising dominion over the paper document that represented that interest (see Pierpoint v Hoyt, 260 NY at 29). Now, however, it is customary that stock ownership exclusively exists in electronic format.

It can be seen that Debiting Payables is a reduction in liability, whereas crediting purchase returns is a decrease in expense. In the case of purchase returns, it can be seen that goods are returned to the supplier and subsequently recorded in General Ledger under the account of Purchase Returns. When a customer returns something they paid for with credit, your Accounts Receivable account decreases. Reverse the original journal entry by crediting your Accounts Receivable account.

The goods have a sales value of 1,000 and had been sold to the customer on account, the balance due remains outstanding in the accounts receivable (trade debtors) account of the customer. Post an accounting entry for purchase returns in the books of Unreal Corporation. The company may grant a reduction of the purchase price to customers so that customers can keep the goods.

Leave A Comment